General Studies- III (Indian Economy)

Editorials In-Depth

09 April 2021

Keeping policy rates unchanged, the Reserve Bank of India, recently, sought to quell the concerns of market participants over rising bond yields.

- Reiterating the RBI’s commitment to maintaining the current accommodative policy stance until the economy is back on track, the Governor enthused the markets with a new programme — Government Securities Acquisition Programme (G-SAP).

- Through G-SAP it will purchase government securities worth Rs 1 lakh crore in the first quarter of FY22.

- The RBI also announced that it will continue with a variable rate reverse repo to suck excess liquidity.

What is G-SAP and how is it different from a regular bond purchase?

The RBI periodically purchase Government bonds from the market through Open Market Operations (OMOs).

- The G-SAP is in a way an OMO but there is an upfront commitment by the central bank to the markets that it will purchase bonds worth a specific amount.

- The idea is to give a comfort to the bond markets. In other words, G-SAP is an OMO with a ‘distinct character’.

What is target of this exercise?

The plan is to enable a stable and orderly evolution of the yield curve amidst comfortable liquidity conditions.

- The endeavour will be to ensure congenial financial conditions for the recovery to gain traction.

- Also, the positive externalities of G-SAP 1.0 operations need to be seen in the context of those segments of the financial markets that rely on the G-sec yield curve as a pricing benchmark.

Is the plan working?

It appears so.

- The 10-year G-Sec yields have responded positively to the RBI’s announcement with the yields on the benchmark paper easing to 6.03 percent from 6.08 percent April 7.

- Dealers said the central bank’s upfront commitment has soothed the market sentiments.

Who benefits?

Mainly the government.

- It has a massive borrowing programme scheduled for FY22.

- The RBI’s endeavor is to keep the yield down to lower the borrowing cost of the Government.

- The Government has planned a Rs 12.05 lakh crore borrowing plan for fiscal year 2022.

Is the RBI keeping the yield down a good idea?

For the Government, it is a good news because the overall borrowing costs go down.

- But, a section of economists aren’t comfortable with RBI artificially keeping the interest rates lower in the financial system as it will lead to distortions.

- In healthy economic system, the interest rates pricing should be driven by demand-supply, and shouldn’t be artificially suppressed by the central bank.

Consequences:

It will have other consequences. Such as: When the RBI is adamant to signal lower rates no matter what happens to support the Government borrowing, it will influence the financial system.

- Cheaper rates will be good news to big, top rated companies who can issue bonds to raise money and to the government.

- But low interest rates coupled with high inflation is a systemic worry for savers.

- Already, savers are getting negative returns on their deposits if one takes into account the inflation adjusted rates or real rates.

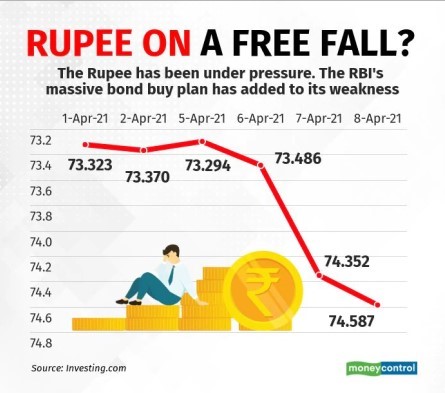

Will it have an impact on Rupee?

Government resorting to massive bond purchase to keep the rates low is not good news for the local currency as it will be under pressure.

- The Indian Rupee came under pressure after the RBI announced the massive Rs one lakh crore bond purchase programme, falling to 74 against the American dollar on April 7.

- Economists say the fear of investors pulling capital out of India in a low interest environment is hurting the local unit.

What are Open Market Operations?

OMOs are the market operations conducted by the RBI by way of sale and purchase of G-Secs to and from the market with an objective to adjust the rupee liquidity conditions in the market on a durable basis.

- When the RBI feels that there is excess liquidity in the market, it resorts to sale of securities thereby sucking out the rupee liquidity.

- Similarly, when the liquidity conditions are tight, the RBI may buy securities from the market, thereby releasing liquidity into the market.

RBI carries out the OMO through commercial banks and does not directly deal with the public.

Types of Open Market Operations:

RBI employs two kinds of OMOs:

- Outright Purchase (PEMO): this is permanent and involves the outright selling or buying of government securities.

- Repurchase Agreement (REPO): this is short-term and are subject to repurchase.

Source: The Hindu / Moneycontrol